Growth Stock Could Keep Soaring")

Semiconductor specialist Cirrus Logic (NASDAQ: CRUS) may not be a household name like some of its industry peers, but the company has done impressively well on the market so far this year with gains of 69% as of this writing.

Cirrus, which is known for supplying chips for Apple‘s (NASDAQ: AAPL) products, has outpaced the broader Nasdaq-100 Technology Sector index’s gains of 10% by a big margin. The good news is that Cirrus’ outstanding growth is here to stay, and the company could finish the year strongly thanks to its largest customer. What’s more, the arrival of artificial intelligence (AI)-enabled smartphones is likely to unlock a massive long-term growth opportunity for Cirrus Logic.

Let’s take a closer look at the reasons why investors should consider buying Cirrus Logic stock hand over fist before it’s too late.

Cirrus Logic’s recent results point toward a bright future

Cirrus Logic released fiscal 2025 first-quarter results (for the three months ended June 29) on Aug. 6. The company’s revenue increased 18% year over year to $374 million and was well ahead of the consensus estimate of $318 million. What’s more, Cirrus’ adjusted earnings jumped a solid 67% year over year to $1.12 per share, crushing Wall Street’s $0.61 per share estimate.

The positive news didn’t end here, as Cirrus expects its fiscal Q2 revenue to land between $490 million and $550 million. The midpoint of the guidance range stands at $520 million, and that’s well above the Wall Street estimate of $485 million. Cirrus clocked revenue of $481 million in the same quarter last year, indicating that its top line is on track to increase by 8% on a year-over-year basis.

Cirrus’ top line could land closer to the higher end of its guidance range thanks to its largest customer, Apple, which accounted for a whopping 88% of its top line last quarter. Cirrus management pointed out on the recent earnings conference call that its revenue exceeded the top end of its original guidance range thanks to “stronger than expected shipments into smartphones.”

Because Apple is Cirrus’ largest customer, the stronger-than-expected performance means that Cirrus got more orders for its chips last quarter. That’s not surprising, as Apple seems to be preparing for an aggressive rollout of its next-generation iPhones that are all set to support generative AI features.

Apple’s rumored iPhone 16 is expected to hit the market next month and the tech giant is expected to ship 90 million units of its updated smartphone lineup this year. That would be a 10% increase over last year. But at the same time, supply chain reports indicate that Apple is stocking up on 120 million display panels, suggesting that it may end up manufacturing more units than what the market is currently anticipating.

If that’s indeed the case, Cirrus Logic’s growth in the current quarter is likely to exceed expectations once again. But more importantly, the integration of the Apple Intelligence suite of generative AI features into the tech giant’s upcoming smartphones is expected to trigger a solid upgrade cycle. Apple’s smartphone shipments are expected to increase by 10% in fiscal years 2025 and 2026, according to JPMorgan‘s estimates.

Cirrus is expected to land more dollar content in the next generation of iPhones, which means that it should be able to receive more revenue from each unit of the iPhone that Apple produces. So, the stage seems set for Cirrus Logic to end the year strongly, and it should be able to sustain its newly found momentum in the future as well thanks to Apple’s entry into the AI smartphone market, a space that’s currently in its early phases of growth.

A couple more reasons to buy the stock

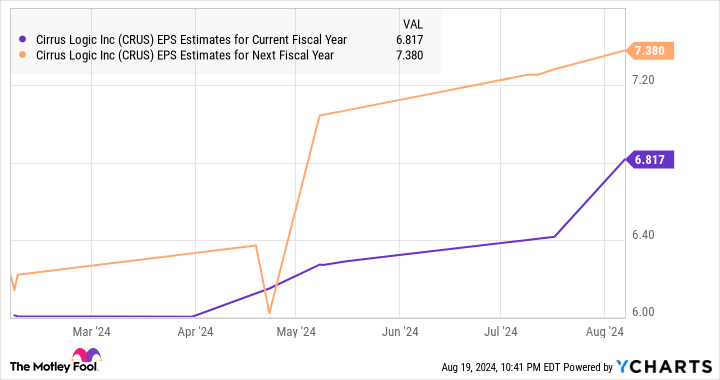

Analysts have been quick to raise their earnings growth expectations for Cirrus Logic, as is evident from the chart below.

Cirrus Logic finished fiscal 2024 (ended on March 30) with non-GAAP earnings of $6.59 per share. The above chart tells us that analysts weren’t expecting an increase in Cirrus’ earnings in the current fiscal year, but that has changed of late. Additionally, the company’s bottom-line growth forecast for the next fiscal year points toward an improvement in its growth rate.

However, if Apple indeed decides to ramp up the production of its upcoming iPhones and Cirrus ends up supplying more content to the tech giant, there is a good chance of Cirrus’ earnings easily outpacing analysts’ expectations going forward.

That’s why now would be a good time for investors to buy this semiconductor stock. It’s trading at just 26 times trailing earnings, a discount to the Nasdaq-100 index’s earnings multiple of 31. And the AI-driven growth in the smartphone market and Cirrus’ tight relationship with one of the largest players in this space could lead to better-than-expected growth going forward.

Should you invest $1,000 in Cirrus Logic right now?

Before you buy stock in Cirrus Logic, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Cirrus Logic wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $792,725!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 22, 2024

JPMorgan Chase is an advertising partner of The Ascent, a Motley Fool company. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple and JPMorgan Chase. The Motley Fool recommends Cirrus Logic. The Motley Fool has a disclosure policy.

Up 69% in 2024, This Red-Hot Artificial Intelligence (AI) Growth Stock Could Keep Soaring was originally published by The Motley Fool

Jessica Roberts is a seasoned business writer who deciphers the intricacies of the corporate world. With a focus on finance and entrepreneurship, she provides readers with valuable insights into market trends, startup innovations, and economic developments.