While the market continues to march higher, with the S&P 500 repeatedly hitting new all-time highs, there is at least one subsector of the market that is greatly undervalued compared to where its stocks have traded historically. That would be the energy midstream sector.

Even better, the midstream industry as a whole is in much better shape today compared to a decade ago when the stocks in it traded at much higher valuations. Let’s take a look at the dynamics of the industry and some stocks in the sector that look poised to outperform over the next several years.

The midstream sector of the energy industry

While the companies in the midstream space are best known for their pipeline assets, they perform a variety of tasks in the energy complex. This ranges from gathering crude and natural gas at the wellhead to separating the hydrocarbons (such as processing and fractionation) to providing water delivery and disposal (fracking requires a lot of water). It also manages storage, long-haul transport, marketing, compression, and other services.

Midstream companies tend to favor fee-based contracts, where they take on no commodity and assume no spread risk. And when new projects are built they often come with take-or-pay provisions, where the company gets paid whether its services are used or not, or minimum volume commitments (MVCs), where the midstream company gets deficiency payments if a customer does not use all its volume capacity.

Some contracts still come with price components that let midstream companies participate in commodity price upside as well, usually on the natural gas and natural gas liquid (NGL) side of the business. For example, with a percentage-of-proceeds contract a midstream company will sell residue gas and/or NGLs into the market on behalf of a producer and retain a percentage of the sale. Another type of contract are keep-whole arrangements, where natural gas processors keep the NGLs that are taken out but must replace them with an equivalent amount of gas on a BTU basis. This exposes a company to changes in the prices between NGLs and natural gas.

The trend in recent years, though, has favored fee-based contracts, which provide these companies with a lot of visibility. And while there is volume risk, this is usually somewhat mitigated by take-or-pay and MVC provisions. Having assets tied to demand centers or stronger basins also helps lessen risk, as utility power demand tends to remain strong while basins with better economics tend to hold up better during periods of lower prices.

Meanwhile, with energy demand coming from data centers given the boom in artificial intelligence (AI), companies involved in natural gas transport look well positioned to benefit from the current AI wave. Goldman Sachs recently predicted that data center power demand will grow 160% by 2030, which will lead to 3.3 billion cubic feet per day of new natural gas demand.

Utilities will need to invest in new generation capacity, and new pipelines will be needed to support this growth. Midstream companies with well-established systems around places with cheap natural gas supplies, such as the Permian and Appalachia, will be the best positioned to benefit.

Low historic industry valuations

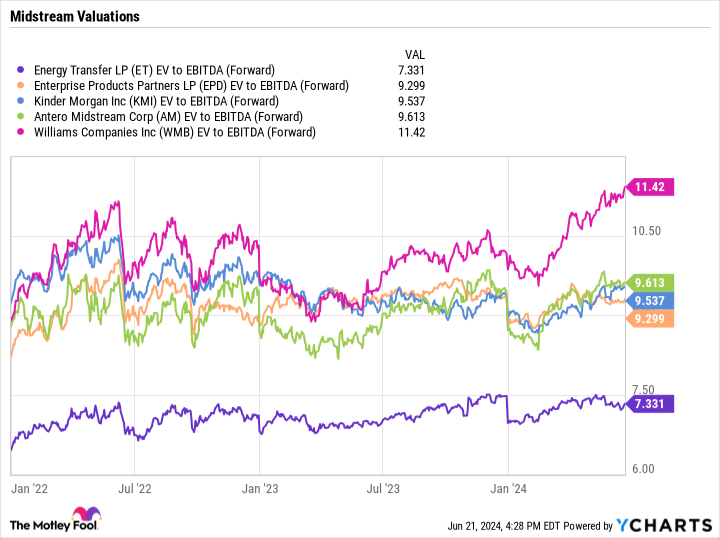

Between 2011 to 2016, midstream companies on average traded at an enterprise value (EV)-to-EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 times. This is one of the metrics most commonly used to value these companies, as it takes into consideration their net debt and the depreciation expenses associated with building out pipelines. Today, multiples throughout the industry are much lower.

The ironic thing is that the companies in the space are in much better shape today than they were during that period. Leverage (debt divided by EBITDA) is down significantly within the industry, while distribution coverage ratios are up and midstream companies are generally generating strong free cash flow.

It is also worth noting the energy producer (E&Ps) customers of midstream companies tend to be in better financial shape, helping reduce customer risk, and the industry has turned its focus on free cash over previously chasing volumes.

Midstream stocks set to outperform

Historically low valuations combined with better financial health and strong growth stemming from increased natural gas demand from AI sets the industry up to potentially return to the valuation levels these stocks saw back in their heyday.

Among the top stocks set to benefit are Energy Transfer (NYSE: ET), Enterprise Product Partners (NYSE: EPD), and Kinder Morgan (NYSE: KMI), all of which have large integrated systems and strong presences in the Permian. Williams Companies (NYSE: WMB) is another solid option given its large natural gas pipeline system that goes from the Appalachia region to power demand centers in the Southeast. However, its stock does trade at a premium to its peers.

Of the stocks highlighted above, Energy Transfer stands out for its low valuation and growth prospects and is my favorite stock in the space. It and Enterprise also have the most attractive yields of the group at 8.1% and 7.2%, respectively.

A more under-the-radar name that could benefit is Antero Midstream (NYSE: AM), which has noted how much data center power consumption demand the Marcellus shale region and its primary customer, Antero Resources (NYSE: AR), have been seeing. Antero Midstream is a well-run natural gas gathering operation servicing Antero. It is benefiting from rebate roll-offs (it previously gave Antero Resources a price rebate when natural gas pries were low) and looks poised to start increasing its distribution in the future.

Energy Transfer, Enterprise, Kinder Morgan, and Antero Midstream all trade at forward EV/EBITDA multiples of less than 10, while Williams trades at under 11.5.

Given the opportunities in front of them and where they trade today versus historical valuations, these undervalued stocks could be among the best-performing value stocks over the next several years.

Should you invest $1,000 in Energy Transfer right now?

Before you buy stock in Energy Transfer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Energy Transfer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $723,729!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 24, 2024

Geoffrey Seiler has positions in Energy Transfer and Enterprise Products Partners. The Motley Fool has positions in and recommends Goldman Sachs Group and Kinder Morgan. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.

Prediction: These Could Be the Best-Performing Value Stocks Through 2030 was originally published by The Motley Fool

Jessica Roberts is a seasoned business writer who deciphers the intricacies of the corporate world. With a focus on finance and entrepreneurship, she provides readers with valuable insights into market trends, startup innovations, and economic developments.