(Bloomberg) — When a Walgreens Boots Alliance Inc. affiliate bought Summit Health-CityMD around a year ago, the pharmacy group’s management hailed the deal as transformational for its push into primary health care.

Most Read from Bloomberg

Twelve months later, the $8.9 billion takeover has struggled to deliver cost synergies and Walgreens’s creditworthiness has just been cut to junk for the first time since its formation.

The travails highlight a problem facing companies that relied on cheap credit to fund big mergers and acquisitions during the boom times: how to keep lofty M&A promises while servicing large debt loads in a new environment of higher rates and fading consumer demand.

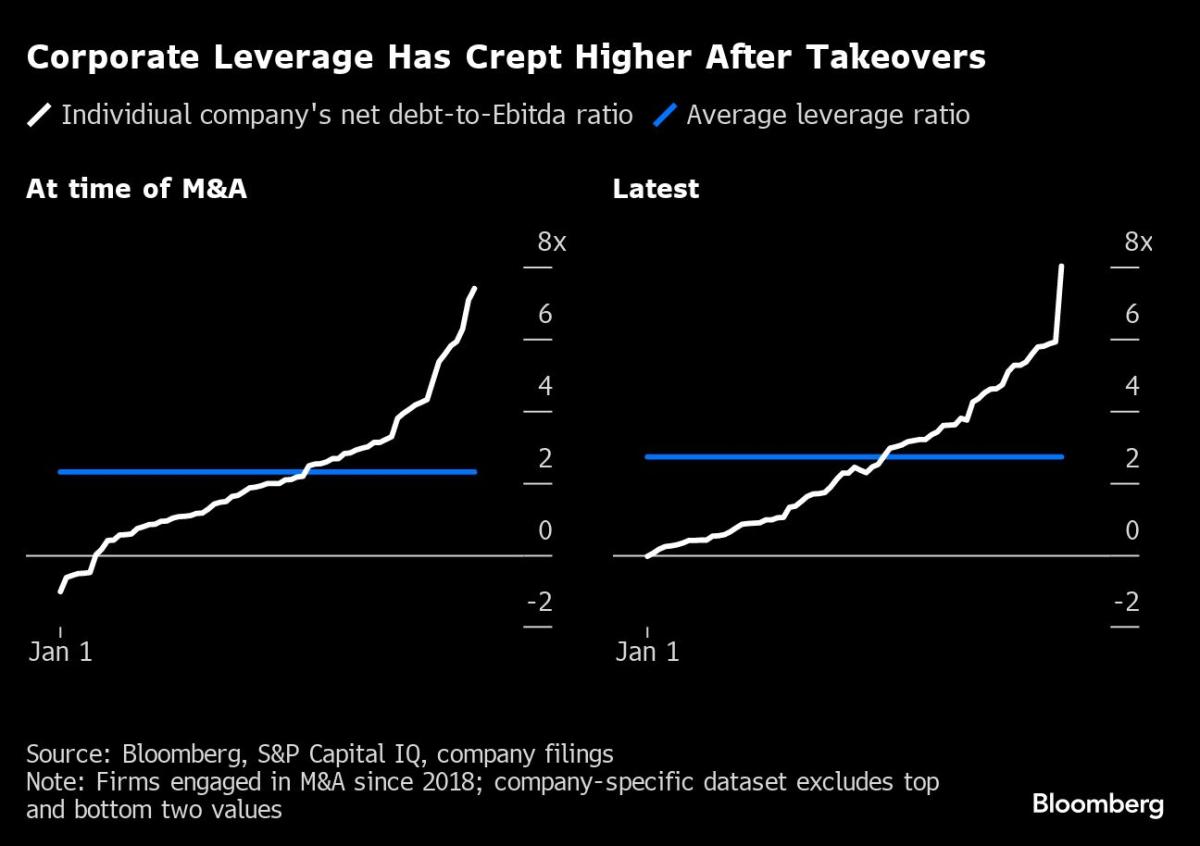

Bloomberg News delved into company filings, bond indexes and ratings agency reports in an analysis of 75 of the largest corporate acquisitions over the past five years with a combined value of almost $1.3 trillion.

The search found that:

-

Less than half of the companies have managed to cut leverage ratios since their acquisitions

Most Read from Bloomberg

-

Almost a third of the 75 firms have a leverage ratio above 3.5, compared with 16 at the time of the acquisitions, suggesting ratings companies have so far given buyers lots of leeway to deliver savings or to make deals a success

Most Read from Bloomberg

-

Average net debt to earnings before interest, taxes, depreciation and amortization stands at 2.7, compared with 2.4 previously

Most Read from Bloomberg

“Weaker blue-chip firms that could secure relatively cheap funding were doing large, debt-financed M&A transactions that committed them to delevering in the short term, which didn’t materialize,” said Tim Eisert, associate professor of finance at Portugal’s Nova School of Business and Economics.

Research by a team including Eisert has shown that dealmaking by companies in danger of losing their investment-grade status enables them to keep that rating for a longer period of time.Read more: S&P 500 Buyback Programs Near $1 Trillion for 2023 as M&A Flags

Tipping Point

A reckoning may now be coming for corporates that need to refinance debt if they can’t deliver on synergies or earnings growth. And there are plenty of headwinds to contend with: cash buffers built up during the Covid-19 pandemic are beginning to erode, sales are under pressure from weaker consumer spending and the risk of recession threatens future profits.

When post-M&A performance disappoints, debt burdens quickly become a headache for companies and their investors. At fewer companies has this been more evident in recent times than at Bayer AG. The German pharma and agriculture conglomerate last month said it’s weighing a breakup that could undo much of its troubled $63 billion takeover acquisition of Monsanto.

Back at Walgreens, Moody’s Investors Service this month downgraded the drugstore chain’s senior unsecured credit to junk, citing its high debt relative to earnings and risks related to its health-care services push. In October, S&P Global Inc. flagged Walgreens’s challenges in de-leveraging and sustaining strong cash flow generation after a spate of transformative M&A as it cut the company to a notch above junk.

“We are disappointed by Moody’s decision and the limited timeframe given to demonstrate the results of our de-leveraging efforts and planned actions to improve underlying business performance,” said a spokesperson for Walgreens, who pointed to the company’s move to cut debt by $2.6 billion in the past year and measures taken to lower its capital expenditure by about $600 million.

Other companies that embarked on multibillion-dollar M&A in the past five years that have seen their creditworthiness slide to the edge of junk include cable and internet provider Rogers Communications Inc. and scent maker International Flavors & Fragrances Inc., according to Bloomberg’s analysis.

“A rise in interest costs and weakening earnings has led to a drop in interest coverage and higher leverage ratios,” Sriram Reddy, a managing director at investment firm Man GLG, wrote in October. “It may take a few more quarters, but we do think that aggregate spreads will need to reflect this fundamental deterioration.”

Credit investor Oaktree Capital Management has also been sounding the alarm about the deteriorating quality in the loan market for high-yield firms, arguing much of the floating rate debt was issued on the basis of aggressive earnings assumptions that haven’t been achieved.

Cost Controls

With higher interest rates beginning to hurt, only 7% of chief financial officers surveyed by US Bank felt “very confident” about managing the situation. This has put cutting costs and driving efficiencies high on the agenda for CFOs, who, according to the poll published in October, concede it may come at the expense of future growth.

Executives at Walgreens are slashing spending by closing unprofitable locations in their efforts to improve performance and the company is also reviving discussions about a potential exit from its UK drugstore chain Boots, which could be valued at about £7 billion ($8.9 billion), Bloomberg News reported this month. Walgreens had about $8.1 billion of long-term debt at the end of August, down from $10.6 billion a year earlier.

Elsewhere, Rogers CEO Tony Staffieri is looking to reduce borrowings at the combined Rogers-Shaw Communications Inc., having finally completed one of Canada’s biggest-ever corporate takeovers earlier this year. After that deal closed, Rogers was downgraded by S&P to BBB-. The company announced on Dec. 11 the sale of its minority stake in a rival telecommunications firm for more than C$800 million ($598 million), money it will use to trim its debt. Rogers said it expects its debt leverage ratio will be 4.7 times by the end of this year, and that it still plans to divest C$1 billion in other assets — mostly real estate — to bring this down further.

IFF, which in 2019 agreed to buy DuPont de Nemours Inc.’s nutrition and biosciences division for $26 billion, last year outlined a restructuring that included a plan to bring down debt through operational improvements and non-core divestitures. A representative for IFF didn’t respond to requests for comment.

Asset manager Insight Investment expects a difficult operating environment to make debt loads harder to manage for companies, whether interest rates remain high or begin to drop from next year. “There is a strong desire to defend an investment-grade rating,” said Adam Whiteley, head of global credit at Insight. “The next part of the cycle could be more challenging.”

Representatives for Moody’s and S&P declined to comment. A spokesperson for Fitch directed Bloomberg News to a ratings criteria memo posted on its website.

For other recent acquirers, however, the need to navigate higher interest rates and their impact on the consumer doesn’t mean shutting the door on more dealmaking.

Interviews with seven finance executives whose firms engaged in M&A in recent years, including media and entertainment giant Warner Bros. Discovery Inc. and German software company SAP SE, show they continue to seek opportunities. But these are far more likely to be bolt-on than era-defining transactions.

“De-levering and funding growth are not mutually exclusive,” said Fraser Woodford, an executive vice president for treasury at Warner Bros. Discovery. “We are going to reduce debt and grow, not one or the other.” In 2022, Warner Bros. Discovery completed a $43 billion merger with AT&T Inc.’s WarnerMedia division. The company’s debt rating remains unchanged at BBB-.

SAP, meanwhile, is weighing smaller deals having only recently exited the remainder of its stake in Qualtrics International Inc., the software provider it agreed to acquire for around $8 billion five years ago. “Tuck-in acquisitions are always possible,” said Dominik Asam, CFO of SAP. “With higher interest rates usually come declining valuations of M&A targets.”

Waste Management Inc., the trash hauler whose debt- and cash-backed acquisitions in recent years have included buying Advanced Disposal Services Inc. for more than $4 billion, also remains on the lookout for deals, according to its CFO Devina Rankin.

“If the deal is right, we believe that this interest rate environment can still be very attractive because, while elevated compared to the last 15 years or so, it’s certainly still a relatively affordable debt environment,” she said.

Read more: Corporate America Is Ignoring Jay Powell and Bingeing on Debt

Buyers Beware

Some fund managers, including David Brown, co-head of global investment grade at Neuberger Berman Group LLC, are cautious about mistakes previously prudent companies could be about to make with acquisitions as they adjust to the new economic environment.

“Even though interest rates are higher, they’re more optimistic now, so that’s when you start to see activity,” he said. “That’s how you may see downgrades from single-A to triple-B.”

Companies have been paying average premiums of more than 40% to get acquisitions done this year, Bloomberg-compiled data show — one of the highest annual figures on record. To be sure, markets are quick to punish those that fail to justify such big bets.

“There have been very effective deals, but a number of them have been completely value destructive,” said Jan Du Plessis, who was chairman of brewer SABMiller when it was sold in 2016 to Anheuser-Busch InBev at a massive premium.

AB InBev investors haven’t enjoyed the rewards of that $100 billion-plus deal — still one of the largest-ever corporate transactions — with the company’s stock down roughly 50% since the start of 2016.

“People just underestimate the challenges of cultural integration when they do these large deals,” Du Plessis said. “So often they only create value for the selling shareholders.”

Debt-Fueled Dealings

A look at how three deals are currently fairing• Going WellIn 2019, Duke Realty Corp.’s then CFO Mark Denien described Prologis Inc. as a 900-pound gorilla in the world of warehouses. Three years later, Prologis, drawn by Duke’s comparatively new assets in key markets such as New Jersey, acquired its rival in a roughly $26 billion deal.

Prologis expected the deal to generate as much as $370 million in synergies, with a similar amount to potentially come over the longer term. It kept its A rating after the transaction.

“If we can find high quality strategic assets that fit and overlap with our existing portfolio, we’ve come to believe” that “we can just run assets better on our platform,” Prologis CFO Tim Arndt said in an interview, referring to a recent deal to buy properties from Blackstone Inc.

While Prologis is more “disciplined in this environment,” it’s still deploying capital, looking for investment opportunities and developing new assets, according to Arndt. “What we’re really looking for is the spread between the cost of capital and what the deployment can earn,” he said.

Keeping leverage low by real estate standards has given Prologis the option of debt-funded acquisitions. Growth in cash flows as rents for industrial space surged in recent years means the company has struggled with “levering up to perhaps a more optimal number,” Arndt said.

• Work in ProgressOracle Corp. caught some analysts by surprise when it landed its largest-ever acquisition in 2021. Instead of expected debt reductions, the purchase of Cerner Corp. meant the technology group was beginning to look too leveraged for its credit rating.

Major arbiters of creditworthiness had already been quick to cut Oracle’s score in early 2021 when the firm started spending billions of dollars more than expected on share buybacks. Then came the $28 billion-plus acquisition of Cerner, spurring another round of downgrades that left Oracle two steps above the junk threshold.

Before the takeover, Fitch analysts expected debt to drop to 3.2 times earnings by the end of the 2024 financial year. The latest estimates point to higher gross leverage, assuming both earnings grow and debt is repaid. In addition, there’s been some near-term headwinds to Cerner’s growth rate as customers move from license purchases to cloud subscriptions and the business is undergoing modernization.

Executives are working to drive profitability to “Oracle standards,” CEO Safra Catz said on an earnings call in September.

A representative for Oracle didn’t respond to requests for comment.

• A Bitter PillWhen Bayer concluded its deal to buy Monsanto in 2018, the chairman of the German company’s board of management Werner Baumann described the transaction as a great moment for shareholders with the “potential to create significant value.”

The $63 billion deal has instead been a disaster for Bayer, which has encountered an avalanche of US litigation tied to Monsanto products. It’s pledged billions of dollars to resolve lawsuits claiming that the Roundup weedkiller causes cancer, which Bayer denies, and it may have to spend more to handle a growing number of suits linked to legacy Monsanto products, such as toxic polychlorinated biphenyls.

Bayer’s shares have fallen roughly 70% since the Monsanto deal closed, wiping about $70 billion off its market value. The company is now reviewing its strategy under new CEO Bill Anderson, who has said nothing is off the table.

Although Bayer’s purchase of Monsanto falls just outside the parameters of deals done in the last five years for our rankings, it deserves a mention because the firm is now rated BBB by S&P, having been at A- before the deal closed. S&P did revise its outlook on Bayer to positive earlier this year, pointing to higher earnings potential at its crop science and consumer health divisions and declining cash litigation payments.

A spokesperson for Bayer said that regulatory and scientific assessments continue to support the safety of glyphosate — an active ingredient used in Roundup. The spokesperson declined to comment further.

–With assistance from Sabah Meddings, Fiona Rutherford, Derek Decloet, Brody Ford and Tim Loh.

Most Read from Bloomberg Businessweek

©2023 Bloomberg L.P.

Jessica Roberts is a seasoned business writer who deciphers the intricacies of the corporate world. With a focus on finance and entrepreneurship, she provides readers with valuable insights into market trends, startup innovations, and economic developments.