(Bloomberg) — Bond investors who were once convinced that the Federal Reserve would start cutting interest rates this week are painfully surrendering to a higher-for-longer reality and a murky path forward for the market.

Most Read from Bloomberg

Treasury yields spiked in recent days and are on the cusp of setting new highs for the year as data continues to point to persistent inflation, which is causing traders to push back their timetable for US monetary easing.

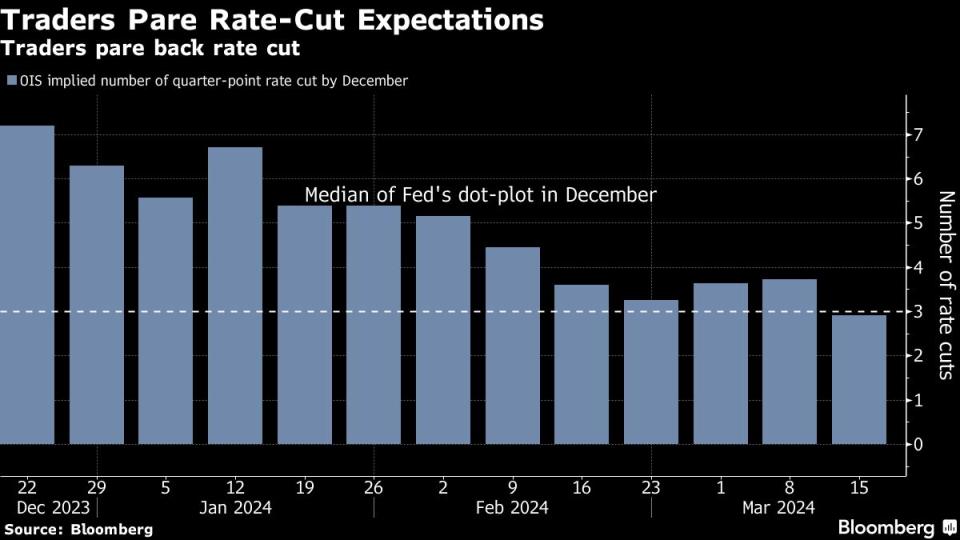

Interest-rate swaps now reflect market expectations for fewer than three quarter-point rate cuts this year. That’s less than the Fed’s median projection in December and a shade of the six reductions that were priced in at the end of 2023. And the first move lower? Investors are no longer confident that it’ll even happen in the first half of the year.

The shift underscores mounting worries that US central bankers led by Fed Chair Jerome Powell may signal an even shallower easing cycle at this week’s two-day gathering, which begins on Tuesday. Already, economists at Nomura Holdings Inc. scaled back their estimate for Fed rate reductions this year to two cuts from three. And recent trading flows in options markets show investors are seeking protection against the risk of higher long-term yields and fewer rate cuts — even if their longer-term view is for rates to eventually come down.

“The Fed wants to ease but the data isn’t allowing them,” said Earl Davis, head of fixed income and money markets at BMO Global Asset Management. “They want to maintain optionality to ease in summer. But they will start to change, if the labor market is tight and inflation remains high.”

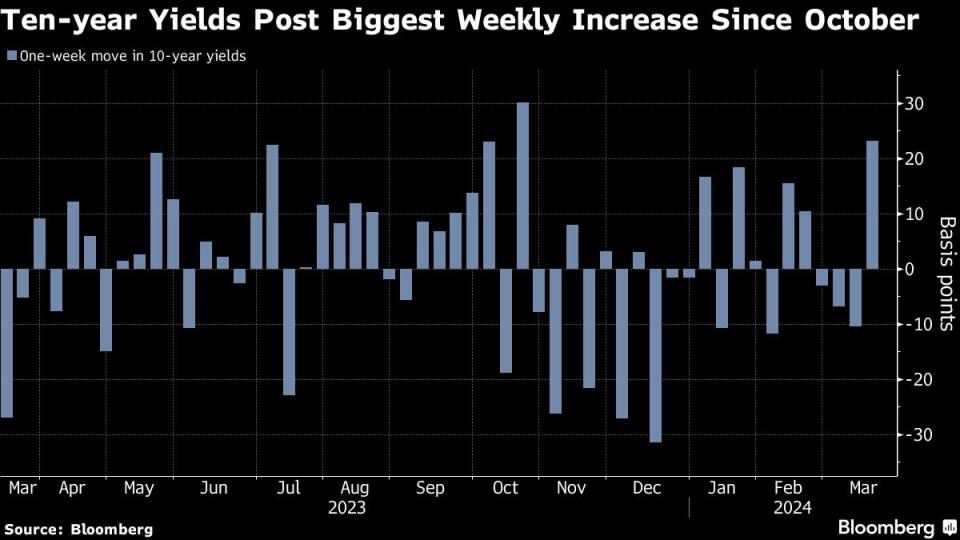

US 10-year yields jumped 24 basis points last week, the most since October, to 4.31% — nearing their year-to-date high of 4.35%. Davis sees 10-year yields rising toward 4.5% a move that would eventually offer an entry point for him to buy bonds. The benchmark rose above 5% last year for the first time since 2007.

Both two- and five-year US yields surged more than 20 basis points, for their biggest rise since May. The selloff extended Treasuries’ losses for the year to 1.84%.

As recently as December, bond traders were all but certain the Fed would start to ease at this week’s meeting. But after a raft of surprisingly strong data on growth and inflation, they see zero chance of action this week, slim odds of a move in May and only a 60% possibility of a cut in June. For the year, traders have penciled in expectations for a total reduction of 71 basis points, meaning a three full-quarter-point cut is no longer seen as guaranteed.

For its part, Nomura now sees the Fed easing in July and December, instead of in June, September and December. “With little urgency to ease, we expect the Fed will wait to see whether inflation is slowing before beginning a rate-cut cycle,” economists including Aichi Amemiya wrote in a note.

The margin to shift the Fed’s median rate projections on its so-called dot-plot is thin. It would take only two policymakers switching to two cuts this year from three for the central bank’s median forecast to move higher.

Read more: Bond Traders Prep for Dot Plot, With Three Cuts in Question

“It’s not going to take a lot” for the median dots to move higher, said Ed Al-Hussainy, a rates strategist at Columbia Threadneedle Investment. “What I am nervous about is the front end of the curve. It’s super-sensitive to the near-term policy path.”

Even if 2024 median rate projections remain intact, the dots in 2025 and 2026 as well as the long-term “neutral” rate — the level seen as neither stoking growth or holding it back — may move higher, a scenario will prompt traders to price in less rate reductions, according to Tim Duy, chief US economist at SGH Macro Advisors LLC.

“We don’t think market participants need to wait for the Fed’s permission” to price in less cuts, wrote Duy. If the two-cut scenario doesn’t materialize this week, it may come by the June meeting, “or at least that market participants will price it as coming by June,” he added. “The risks at this moment are decidedly asymmetric.”

What Bloomberg Intelligence Says …

“Changes are likely to be incremental, though the knee-jerk reaction to a move higher in the 2024 dot may be quickly discounted if the 2025 dots are largely unchanged. …the market is sensitive to the end of next year dots, meaning rate markets may focus on 2025.”

— Ira Jersey, chief US interest-rate strategist

Instead of sweating over two or three reductions, investors shouldn’t lose the big picture that the Fed’s next move is a cut, not a hike, said Baylor Lancaster-Samuel, chief investment officer at Amerant Investments Inc. That means it’s time to buy bonds and take the interest-rate, or “duration” risk, in Wall Street parlance.

“You can debate the timing, but in our opinion, the Fed is still likely to cut sometime this year,” said Lancaster-Samuel. “In that environment, we think the level of rates does not have too much risk of ratcheting higher from here. So we believe the opportunity cost of not taking duration is higher than the risk of taking it.”

Options traders are less sanguine. On the heels of last week’s stronger-than-expected data on producer prices, traders rushed to buy hawkish protection for this year and next in options linked to the Secured Overnight Financing Rate, a measure which closely tracks the central bank policy rate.

“Higher inflation readings, coupled with outsize deficits, the potential for the Fed to remain on hold longer, lends itself to another move toward the 2023 yield highs,” said Gregory Faranello, head of US rates trading and strategy for AmeriVet Securities.

What to Watch

-

Economic data:

-

March 18: New York Fed services business activity; NFIB housing market index

-

March 19: Building permits; housing starts; TIC flows

-

March 20: MBA mortgage applications; FOMC meeting

-

March 21: Current account balance

-

March 21: Philadelphia Fed business outlook; initial jobless claims; S&P Global US manufacturing PMI; leading index; existing home sales

-

-

Fed calendar:

-

March 21: Vice Chair for Supervision Michael Barr

-

March 22: Chair Jerome Powell, Vice Chair Philip Jefferson and Governor Michelle Bowman at Fed Listens event; Barr; Atlanta Fed President Raphael Bostic

-

-

Auction calendar:

-

March 18: 13-, 26-week bills

-

March 19: 52-week bills; 42-day cash management bills; 20-year note re-opening

-

March 20: 17-week bills

-

March 21: 4-, 8-week bills; 10-year TIPS re-opening

-

—With assistance from Edward Bolingbroke.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Jessica Roberts is a seasoned business writer who deciphers the intricacies of the corporate world. With a focus on finance and entrepreneurship, she provides readers with valuable insights into market trends, startup innovations, and economic developments.