(Bloomberg) — Inflation in the US probably abated only gradually last month and retail sales rebounded, illustrating why the Federal Reserve is in no rush to lower interest rates.

Most Read from Bloomberg

The core consumer price index, a measure that excludes food and fuel for a better picture of underlying inflation, is seen rising 0.3% in February from a month earlier after a 0.4% advance to start the year. The Labor Department will issue its CPI report on Tuesday.

The price gauge is projected to have risen 3.7% from a year ago, which would mark the smallest annual advance since April 2021. While the year-over-year figure is well below the 6.6% peak reached in 2022, the pace of progress more recently has been modest.

That squares with congressional testimony from Fed Chair Jerome Powell in the past week, who said that while it would likely be appropriate to cut rates “at some point this year,” he and his colleagues aren’t ready yet.

Read more: Powell Says Fed ‘Not Far’ From Confidence Needed to Cut Rates

That’s because the Fed wants convincing signs that inflation is nearing their 2% target, based on a separate gauge — the personal consumption expenditures price index. In addition to the CPI, the government’s producer price index on Thursday will help inform the PCE index, which will be released after the US central bank’s March 19-20 policy meeting.

Fed officials will observe a blackout period for speaking engagements ahead of that meeting.

Away from inflation, there are scant signs of stress in the economy. The latest jobs report pointed to moderating yet healthy employment growth that will keep consumer spending afloat.

Government figures on Thursday are expected to show a 0.8% advance in February retail sales following a drop of the same magnitude a month earlier. Such an outcome would indicate a return of shoppers who took a breather after a strong holiday-shopping season.

Other US data in the coming week include February industrial production and the University of Michigan’s preliminary March consumer sentiment index.

Turning north, national balance sheet data from Canada will offer a look at household finances as high interest rates weigh on heavily indebted mortgage-holders.

What Bloomberg Economics Says:

“February’s CPI report is unlikely to provide the reassurance Powell needs to adopt a firmly dovish stance. Seasonal trends observed in the January report, which drove up core CPI, are expected to persist in February. We think it’s a close call between May or June for the Fed’s first rate cut.”

—Anna Wong, Stuart Paul, Eliza Winger and Estelle Ou, economists. For full analysis, click here

Elsewhere, wages in Japan and the UK, plus a flurry of inflation numbers from Sweden to Brazil, will keep investors busy.

Click here for what happened last week and below is our wrap of what’s coming up in the global economy.

Asia

Japan’s closely watched annual wage negotiations reach a milestone with the release on Friday of the results from the main union group, Rengo.

The numbers are expected to top last year’s results, which were already the best in decades, paving the way for the Bank of Japan to end its negative rate either this month or next.

Also feeding into that rubric will be Japan’s final fourth-quarter gross domestic product statistics on Monday. They’re likely to be revised higher to possibly pull the nation out of a technical recession, in what would be another green light for the BOJ.

Elsewhere, India’s industrial output may have increased at a faster clip in January, while February inflation is seen cooling a tad.

India, Indonesia and the Philippines get trade data in the coming week, and Australia will get the February NAB Business Conditions gauge and household spending numbers.

Europe, Middle East, Africa

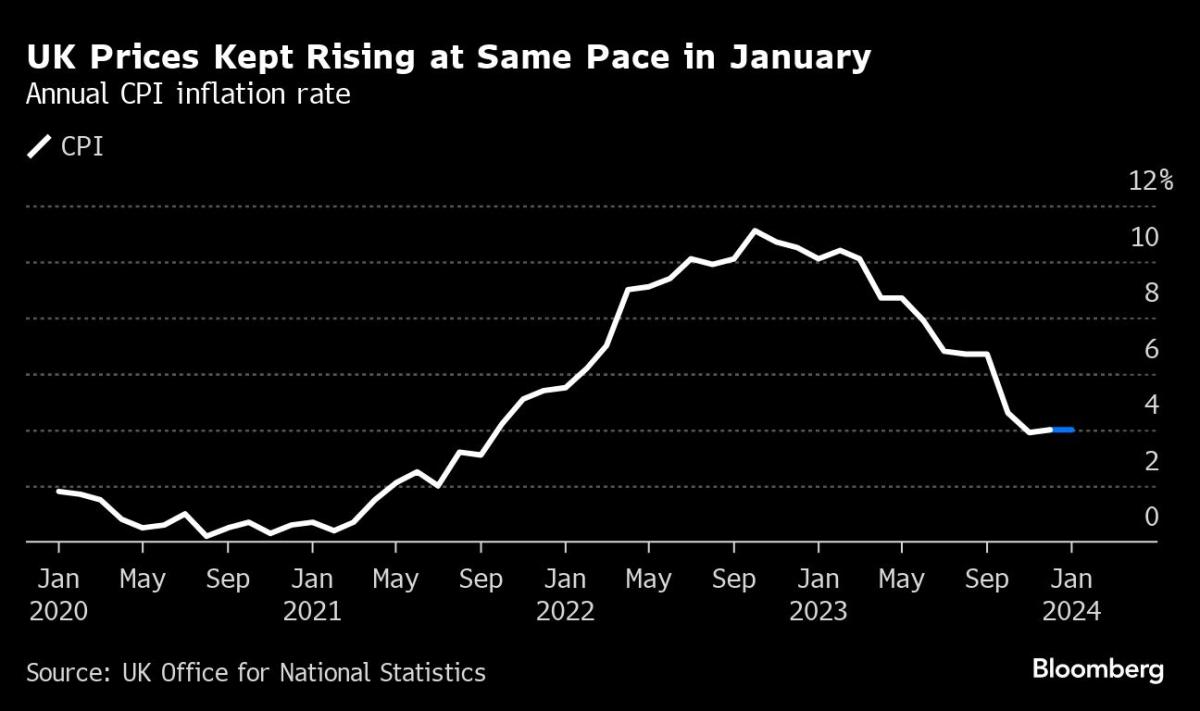

The UK will take center stage in the region, with wage data on Monday likely to show a still-robust pace of increase that will keep the Bank of England wary. In a hint of the labor market’s tightness, the central bank itself has just been forced to grant raises to its staff that match inflation.

On Tuesday, monthly GDP numbers for the UK are expected to show a small increase after a drop in December, underscoring how the economy is still struggling. The BOE will release its own survey of consumer inflation expectations on Friday.

Turning to the euro zone, the main report will be industrial production, which is anticipated to show that 2024 began with a monthly drop.

Meanwhile, following last week’s European Central Bank decision signaling a rate cut in June, several officials are due to speak, including chief economist Philip Lane. The institution may unveil a revamp of its monetary policy framework on Wednesday.

Several European countries will release inflation numbers, including Denmark, Norway, Sweden, Serbia and Romania. And Ukraine’s central bank will announce its latest rate decision on Thursday amid uncertainty over US military aid.

Turning south, data Sunday showed that Egyptian inflation unexpectedly accelerated in February, a trend that may continue after a much-anticipated flotation of the pound aimed at turning around the troubled economy. The data will follow the central bank’s jumbo rate hike of 600 basis points and currency devaluation on Wednesday.

In Nigeria, by contrast, data on Friday will likely show price growth past 30% as it struggles in the aftermath of a currency devaluation.

On the same day, Angola is expected to increase its key rate to stem upward pressure on inflation from adverse weather conditions and a weaker exchange rate.

Also on Friday, Israel will report inflation. Price growth has slowed sharply in the past year to 2.6%, even with the onset of the war against Hamas in October. The Bank of Israel has still avoided rate cuts amid uncertainty about the duration of the conflict, already into its sixth month, and its impact on prices.

Latin America

The Brazilian central bank’s survey of economists gets the week rolling on Monday. Inflation expectations for year-end 2024 have been inching down but those for the following three years remain unmoored.

Local economists see consumer price increases slowing to 3.76% by year-end, a shade below estimates from economists surveyed by Bloomberg. Data posted Tuesday will likely show that annual inflation slowed back to within policymakers’ 1.5% to 4.5% target range.

Retail sales in Brazil disappointed in December amid an extended softening of consumer confidence that may also weigh on January figures due Thursday.

Mexico posts January industrial production data after the year-on-year reading flatlined in December. Against that negative, manufacturing and production trend indicators rose for a third month in February to a three-year high.

Peru’s GDP-proxy data for January will likely show the Andean economy leaving 2023 and its second-worst contraction in more than 30 years behind. Still, many analysts see a long stretch of mediocre growth ahead.

In Argentina, inflation likely showed for a second month in February from December’s 25.5% reading, though the implied annual rate is forecast to have pushed up over 280%.

While the combination of recession and President Javier Milei’s fiscal adjustments are cooling price pressures, most analysts see triple-digit annual prints extending well into next year.

–With assistance from Brian Fowler, Piotr Skolimowski, Robert Jameson, Laura Dhillon Kane, Paul Wallace and Monique Vanek.

(Updates with Egypt inflation in EMEA section)

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Jessica Roberts is a seasoned business writer who deciphers the intricacies of the corporate world. With a focus on finance and entrepreneurship, she provides readers with valuable insights into market trends, startup innovations, and economic developments.